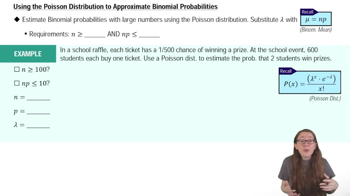

5. Binomial Distribution & Discrete Random Variables

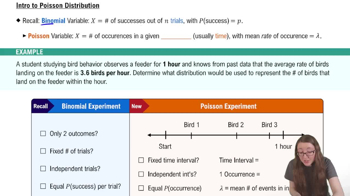

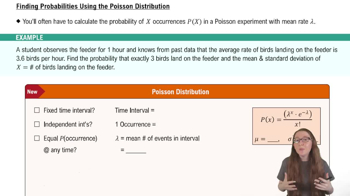

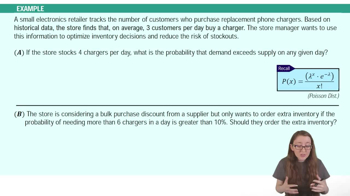

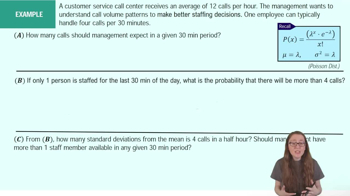

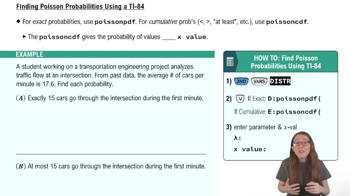

Poisson Distribution

Struggling with Statistics for Business?

Join thousands of students who trust us to help them ace their exams!Watch the first videoMultiple Choice

A financial analyst is assessing the risk of credit defaults in a large bond portfolio. The portfolio contains 2,000 corporate bonds, & the probability of any one bond defaulting in a year is 0.002.

(A) Can the # of bonds which will default be approximated using the Poisson distribution? If so, find .

A

4

B

2

C

The # of bonds which will default cannot be approximated using the Poisson distribution.

Verified step by step guidance

Verified step by step guidance1

The first step is to determine whether the Poisson distribution is an appropriate model for this problem. The Poisson distribution is used to model the number of events occurring in a fixed interval of time or space, under the following conditions: (1) Events occur independently, (2) The probability of an event occurring is the same for all intervals, and (3) The probability of more than one event occurring in a very small interval is negligible. In this case, the defaults of bonds can be considered independent, and the probability of default (0.002) is the same for each bond. Thus, the Poisson distribution is appropriate.

Next, calculate the parameter λ (lambda) for the Poisson distribution. λ represents the expected number of events (defaults) in the given interval (the entire portfolio of 2,000 bonds). It is calculated as the product of the number of trials (n) and the probability of success (p) for each trial. The formula is: .

Substitute the given values into the formula. Here, (the number of bonds) and (the probability of default for each bond). The calculation becomes: .

Simplify the expression to find the value of λ. This represents the expected number of bond defaults in the portfolio over the year.

Finally, interpret the result. If λ is a small value (as expected here), it confirms that the Poisson distribution is a reasonable approximation for modeling the number of bond defaults in this portfolio.

4:00m

4:00mWatch next

Master Introduction to the Poisson Distribution with a bite sized video explanation from Patrick

Start learningRelated Videos

Related Practice